The Kazakhstan deliverable I submitted to ITC in early 2021, under the same Ready4Trade Central Asia project that produced the Kyrgyzstan country research, looked at two priority sectors — home and décor, and food and beverages — and at five priority markets: Northern America, the European Union, Russia, China, and the rest of Central Asia. The findings were presented in a regional Ready4Trade workshop attended by more than a hundred participants — SME founders, national coaches, and programme staff from across Kyrgyzstan, Kazakhstan, Uzbekistan, and Tajikistan.

This post is the record of what that research found. The detailed findings are in the ITC archive. What I want to surface here are the three observations from the Kazakhstan research that did not fit the textbook expectation, and the structural fact that sits underneath all of them.

The structural fact: Kazakhstan has the e-commerce stack the others do not

By 2019, the Kazakh e-commerce market was already 700 billion tenge — a twentyfold increase over the previous decade. In the first half of 2020, despite the pandemic, electronic commerce reached $1.1 billion, on a trajectory to roughly double the previous year. Internet penetration was at 84.2 percent of the population — 18.6 million people. The active online buyer base was 3.2 million users. Sixty-five percent of those buyers made their purchases on smartphones, against a global average of 54 percent.

Underneath the user numbers, the institutional stack was real. The 2017 e-commerce law had registered 579 online shops under a special legal provision that exempted them from income tax. Cashless transaction volume reached 14.4 trillion tenge by 2019 — a 2.3× year-on-year increase. KazPochta, the national postal operator, was running three fulfilment centres with daily shipment volumes of 350,000, and the government had committed to expand to fifteen centres by 2025, projecting 82.8 million annual shipments.

That is not the e-commerce profile of an underdeveloped market. Kazakhstan in 2019 had the indicators of a Central European or Eastern European market that someone had moved to Almaty.

The gravitational centre: Kaspi.kz

The single observation that mattered more than any other was Kaspi.kz. By the time of the research, Kaspi had 4.47 million monthly active users, a product catalogue of 400,000 items, and an October 2020 London IPO that had valued the company at $6.5 billion. That valuation made Kaspi the most valuable digital platform in Kazakhstan by a long margin, and the most valuable home-grown digital platform in any of the Central Asian states. By comparison, Satu.kz — the domestic marketplace runner-up, with 18,000 registered merchants and 6 million monthly active users on its platform — was operating at roughly $3 million in annual turnover.

What Kaspi is, technically, is a super-app: third-largest retail bank in Kazakhstan, fintech and payments rails, online consumer lending, credit cards, money transfer, and a marketplace, all bundled inside a single mobile application. What Kaspi is, for the e-commerce question, is the fact that any Kazakh SME deciding where to sell online has to make a decision about Kaspi first, and about everything else second. The platform’s combination of pre-installed user base, integrated payments, and consumer credit creates a domestic conversion environment that international marketplaces cannot replicate inside Kazakhstan.

The Ready4Trade research recommendation for the domestic side was therefore unambiguous: list on Kaspi, work the listing, treat it as the anchor. Everything else — Satu.kz, Lamoda’s «Made in KZ» category, and standalone .kz storefronts — sat in the second layer.

Lamoda’s Kazakhstan brands

Lamoda had been operating a «Made in KZ» category since 2016, built around domestic fashion and lifestyle producers. By the time of the research, the category listed 18 local brands on the platform — among them Mimioriki, Altezza, and a group of Kazakh apparel labels that had been the early wave of domestic sellers willing to meet Lamoda’s product-photography and fulfilment standards. The category had grown steadily but remained a small corner of Lamoda’s overall Kazakhstan business, where Russian and international brands dominated the volume.

For the Ready4Trade home-and-décor producers in the Kazakh cohort, the Lamoda «Made in KZ» case was a useful illustration: a regional fashion platform had built the infrastructure to accept domestic sellers, had named and publicised the domestic brand programme, and had been running it for five years. The question was not whether the channel existed — it did — but whether décor and craft producers could meet the same listing standards that apparel sellers had already worked out how to meet. The answer for the cohort’s specific producers, in early 2021, was «not yet, but close.»

The SMEs the research was supposed to serve: salt, oil, mare’s milk

The Ready4Trade beneficiaries in Kazakhstan were producers of refined sunflower oil, table salt, and bottled mare’s milk — kumys. Specialised, mostly small, mostly food-and-beverage. The handicraft-and-décor side of the priority sector list included felt slippers, leather goods, traditional ethnic textile, and ornament producers who had a different shape of opportunity entirely.

The food-and-beverage problem was diagnostic-different from the handicraft problem. For handicrafts, the question was whether the products could find international buyers. For Kazakh food and beverage, the question was whether the products matched what international buyers were actually searching for online. The keyword research told a clear story.

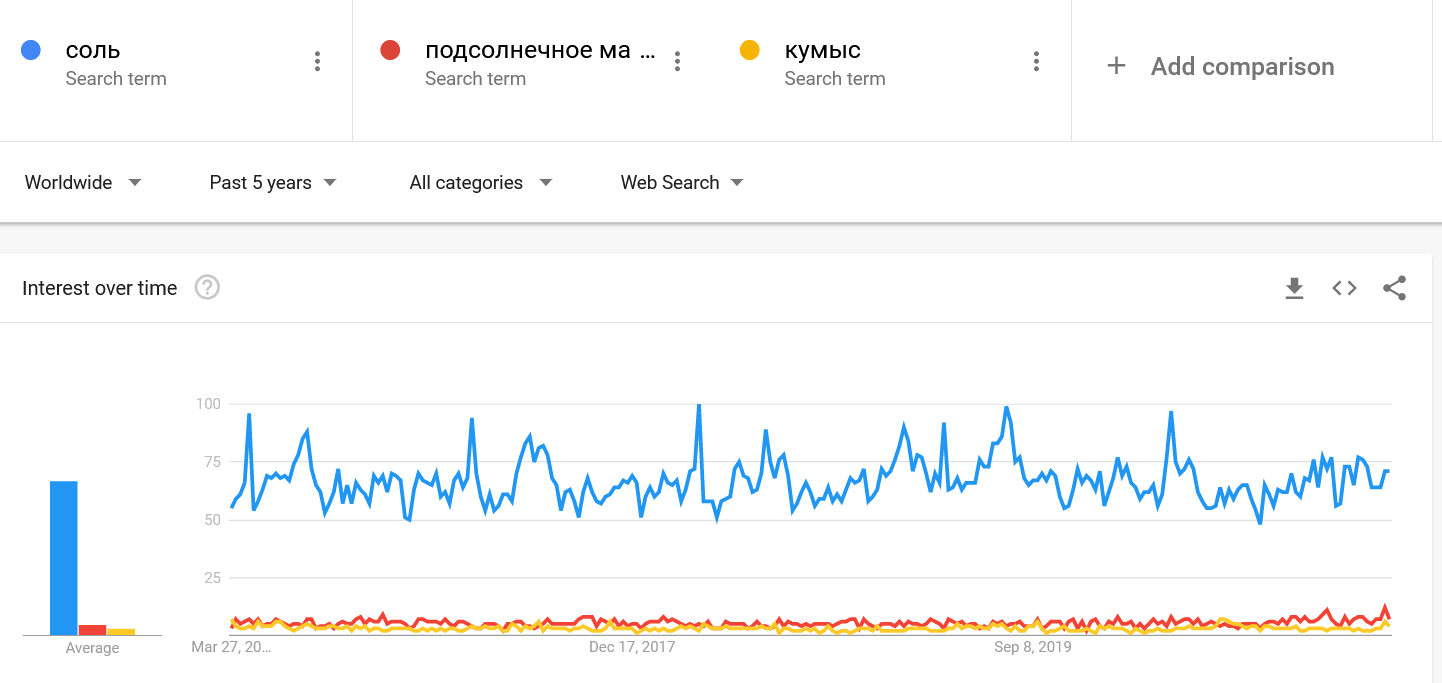

Google Trends data, run against the priority-market keywords for «salt,» «sunflower oil,» «kumys» and «horse milk» in Russian and English, returned essentially flat lines. The international consumer market is not searching for these products as direct-to-consumer e-commerce purchases. The products are real, the producers are real, the export potential is real — but it is not an e-commerce-led export potential. The route to market for Kazakh refined oil is wholesale to retail chains, B2B distribution through grocery import partners, and Alibaba-style supplier-finder platforms (about 200 active Kazakh exporters were registered on Alibaba at the time, of which 43 had upgraded to Alibaba Gold Supplier accounts under a government-supported scheme).

The research recommendation for these SMEs was therefore not «list on Etsy.» It was: build a corporate website with strong English-and-Russian SEO, register on Alibaba, target retail-chain procurement officers, and let the e-commerce platforms support inbound discovery rather than serve as the primary sales channel.

The kumys rabbit hole

One specific observation from the keyword research stayed with me. Searches for kumys — кумыс, mare’s milk — spiked sharply in June and July of 2020 in both Kazakhstan and Russia. The spike was not seasonal demand. It was driven by a specific search-string family: кумыс при пневмонии, кумыс от ковида, как пить кумыс при болезни. People were looking at mare’s milk as a folk treatment for COVID-19.

Whether or not the folk-treatment angle is medically defensible is not the question this research was asking. The question for an SME exporting bottled kumys was: is this spike a real signal of demand the producer could meet, or is it a transient public-fear blip that will not convert to repeat-purchase customers six months later? The honest answer in early 2021 was the latter. Producers should not retool around it. But the more general point — that consumer search behaviour around specific Central Asian foods can spike sharply for non-obvious reasons, and that B2C food-and-beverage SMEs benefit from monitoring those spikes — was a real product of doing this kind of keyword-level research.

The Yandex Wordstat data also showed sustained, non-spike interest in mare’s milk’s health benefits, reviews, and pricing — кобылье молоко отзывы, кобылье молоко при раке, кобылье молоко саумал как пить. That suggested a small but durable B2C demand layer existed, served well by content marketing through YouTube and Yandex’s own search-and-video stack, with a website that converted curious readers into wholesale or sample-pack buyers. That is a different go-to-market model from «list on Wildberries and wait.»

What the report recommended, and what the structure made hard

The final report’s priority-market matrix for Kazakhstan recommended Kaspi.kz and Satu.kz for the domestic layer, Lamoda Market’s «Made in KZ» category for the regional fashion-and-décor layer, Wildberries and Ozon for the cross-border Russian layer, and Alibaba plus a properly-built corporate website for the international B2B food-and-beverage layer. For artisan-side home-and-décor producers, Etsy and Amazon Handmade were on the list — with the same payment-rail caveats that applied in Kyrgyzstan, though Kazakhstan’s regulatory environment was at the time more accommodating to international fintech operators.

What the structure made hard, for the specific Ready4Trade beneficiary SMEs in food and beverage, was the mismatch between the policy goal and the product. The Ready4Trade programme was set up to help small businesses export through e-commerce. The salt and oil producers in the cohort were small businesses with export potential — but their export route ran through wholesale, not through e-commerce, and a research report that says «your sector doesn’t really fit the channel we are funded to help you with» is a difficult report to write. The version I delivered to ITC said it anyway, with the practical alternative — build the corporate website, work Alibaba, treat e-commerce as a discovery and content layer rather than the sales channel — laid out at the same level of detail as the recommendations for the home-and-décor producers.

The Kazakh stack as a baseline

For the Kyrgyz, Uzbek, and Tajik SMEs that were looking across the border at Kazakhstan in early 2021, the Kazakh stack was simultaneously the closest accessible export market and the hardest one to compete inside. The Kaspi user is not a tourist; they are an everyday domestic consumer with a curated set of suppliers already serving them through an integrated app. Selling into Kazakhstan from outside the country was, and still is, the test case for whether regional cross-border e-commerce in Central Asia can be made to work — because if it works into Kazakhstan, it will work everywhere.

Wildberries had announced in 2018 that it would open fulfilment centres in Nur-Sultan and Almaty, with 5,000 jobs by end of 2022. As of January 2021, when the research was written up, no update on those centres had surfaced. Wildberries.kz was running at 3.95 million monthly website visitors with 21 named Kazakh manufacturers selling on it. The infrastructure promise was there; the operational follow-through had not yet materialised. That gap — announced ambition versus delivered platform — was one the participating SMEs asked about repeatedly in the workshop session.

That structural conclusion of the Kazakhstan research — the gap between the domestic stack’s strength and the cross-border route’s immaturity — is what the next phase of the Ready4Trade work would have to navigate.

— Aziz Soltobaev, KG Labs, September 2021.