The handicrafts deliverable I produced for ITC in early 2021, alongside the main Kyrgyzstan country report, was a narrower brief: look only at the handicraft sub-sector — felt, embroidery, traditional ornaments and toys, leather goods, the artisan products that the Ready4Trade programme had identified as having the highest potential and the highest vulnerability inside Kyrgyzstan.

The broader country research had already established the headline: 662 Etsy listings for the keyword Kyrgyzstan, all held by merchants registered outside Kyrgyzstan, and a four-million-dollar Brooklyn company, Craftspring, built entirely on Kyrgyz felt. That structural picture — Kyrgyz production, foreign storefront — is the context for this report. What the specialised handicrafts brief added was a closer reading of why the domestic producer side looked the way it did, and what a realistic path toward changing it would require.

The value chain that collapsed in 2020

The Kyrgyz handicraft economy in 2020 was a value chain that ran in two directions and did not meet in the middle.

In one direction, rural women artisans — concentrated in Naryn, Talas, Issyk-Kul, At-Bashy, and other handicraft-active regions outside Bishkek — produced hand-embroidered felt, shyrdaks, ala-kiyiz, leather goods, and a smaller volume of contemporary-design adaptations. The raw materials were locally-sourced merino wool, locally-available leather and yarn. The work was paid at piece rates set by intermediaries.

In the other direction, the buyers — souvenir boutiques in Bishkek and tourist destinations along the Issyk-Kul belt, bazaar traders at Osh and Dordoi, and a small number of international wholesale partners — sourced from those intermediaries and sold to the end customer, who was overwhelmingly a foreign tourist visiting Kyrgyzstan in the summer-and-winter peak seasons.

The two directions met at the intermediary. The intermediary captured the margin between the piece rate paid to the artisan and the wholesale or retail price paid by the tourist. The pandemic in 2020 broke the tourist side of that exchange completely. Foreign-tourist arrivals collapsed. The intermediary inventories sat on the shelf. The piece-rate income stopped reaching the rural producers.

That was the context. The research question was whether e-commerce channels could pick up the demand the tourist channel had lost.

The logistics geography that made the rural pathway hard

One of the structural findings of the handicrafts brief that did not appear in the broader country research was the geography-of-logistics problem for rural producers specifically.

If a craftswoman in Naryn or Talas wanted to ship a finished felt product to an international customer — through DHL, FedEx, EMS, or the national operator KyrgyzPostasy — she had to physically travel to the central office of those operators in Bishkek. There was no last-mile pickup outside the capital. There was no regional drop-off point. The Eurasian Union destinations had somewhat better coverage through DPD, Pony Express, and SDEK, which delivered into Russia, Kazakhstan, and Belarus from Bishkek. But for an order destined for the United States or the European Union, the operational shape was: artisan finishes the product, intermediary collects from the village, intermediary travels to Bishkek, parcel dispatched, parcel arrives several weeks later.

This logistics geography is one of the practical reasons that the Craftspring model works at scale while the artisan-direct-to-customer model does not. Craftspring buys from intermediaries inside Kyrgyzstan, ships in consolidated wholesale containers to a fulfilment centre in the United States, and fulfils customer orders from there. The fulfilment-centre side of the operation is what makes the destination-market storefront economically possible. Inside Kyrgyzstan, there is no equivalent infrastructure for the rural-producer-to-international-buyer pathway.

What contemporary design opened up

The Craftspring case study — covered in the main country research — is worth returning to from a different angle here: the design-adaptation question.

Craftspring’s product range is technically hand-embroidered felt made by Kyrgyz artisans using traditional techniques. The design is contemporary: New York taxi ornaments, San Francisco trolley ornaments, the late Justice Ruth Bader Ginsburg as a felt figurine, Christmas-market gift items, children’s toys with Western-cultural references. The more recognisably Kyrgyz products — eagle motifs, traditional shyrdak patterns, yurt shapes — are in the range, but they are not the volume drivers.

Imarc Group’s global handicraft market research, which I referenced in the report, identified the shift from ethnic to contemporary designs as one of the key demand drivers globally — pushed by home-and-décor consumption in offices, hotels, hospitals, and by Gen-Z consumers furnishing first apartments and buying gift items online. The Craftspring model demonstrates what that shift looks like in practice for a Kyrgyz-felt product line. Traditional techniques, adapted design.

The design-adaptation question matters for the domestic producers who were in the research. Tumar Art Group and Kiyiz Group were both producing contemporary-adjacent ranges alongside traditional pieces by 2020. Aizada Imports and Datka were operating with more traditional product mixes. The research recommended that all of them treat the contemporary-design shift not as a departure from craft identity but as a market-access tool — because the distribution it opens (US gift retailers, EU home-and-décor chains, online platforms with Western consumer bases) is not accessible to traditional-only product lines at volume.

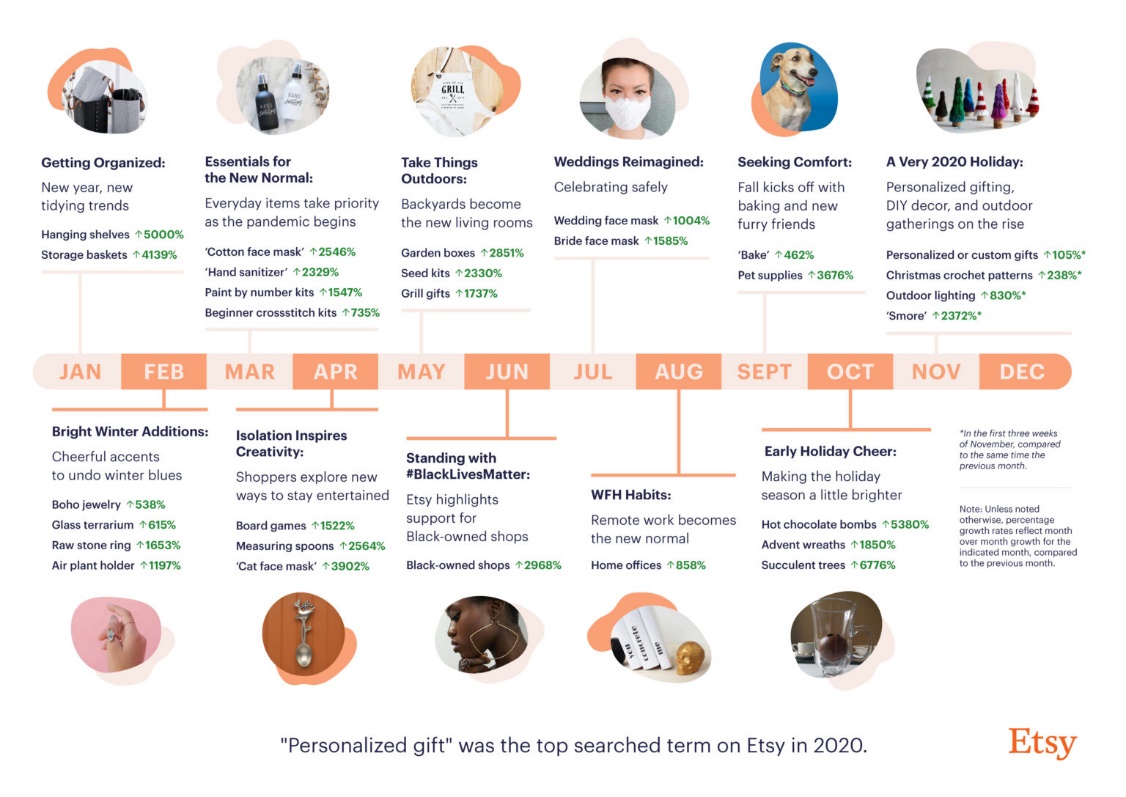

What was happening on Etsy in 2020

The Etsy 2020 Year-in-Search report, which I pulled into the handicrafts research as a demand signal reference, showed how fast consumer preferences had moved during the pandemic year. Searches for home décor had grown 47 percent year-on-year. Searches for gifts for her in personalised and handmade categories were up sharply. The hot chocolate bomb trend — a confectionery category — had grown 5,380 percent, which is an extreme case, but it illustrates the speed at which consumer demand on the platform could shift.

For the handicraft sub-sector specifically, the relevant trend was cosy home and hygge aesthetic searches, which aligned with the felt and textile categories that Kyrgyz producers were already making. The market was there. The Kyrgyz producers were not visible in it.

The producer layer inside Kyrgyzstan

The largest Kyrgyz-resident handicraft producer with international reach at the time of the research was Tumar Art Group, with B2B distribution relationships in multiple countries and a domestic retail network. Tumar’s website, tumar.com, had fewer than 2,000 monthly unique visitors at the time of the research. At the 2019 industry-average e-commerce conversion rate of 4.01 percent for arts and crafts, that produces about 80 sales leads per month and a smaller number of completed orders.

Kiyiz Group was the only Kyrgyz brand with a notable presence on the domestic marketplace Svetofor.info, alongside a limited export footprint. Aizada Imports and Datka were active B2B players in the traditional-mix segment. A handful of others operated through Instagram pages and WhatsApp order fulfilment — a Telegram-based commerce pattern that the research documented but did not quantify reliably.

All of the producers shared the same visibility problem: workable products, websites built on Tilda or WordPress or Bitrix, no functional international payment integration, no automated shipping-cost calculation, limited English-language SEO, and traffic volumes that made the websites commercially inert as standalone sales channels.

What the report recommended

The recommendation matrix for Kyrgyz handicrafts was layered around three routes, given the constraints.

The realistic near-term route for most producers was to build search-engine visibility on their own websites and on B2B marketplaces — FashionGo, Foursource, Qoovee — targeting wholesale buyers who would maintain physical inventory in the destination market and handle the consumer-facing transaction. This route bypasses the payment-rail problem. Wholesale transactions settle through standard bank-to-bank wires. It also accommodates the logistics geography by consolidating shipments into wholesale containers rather than individual parcels.

The medium-term route was to develop a destination-market storefront through partnership or licensing — treating the Craftspring model not as a competitor pattern but as a structural template, and asking whether a Kyrgyz cooperative could operate a US-registered or EU-registered storefront under shared ownership, with the value-capture rebalanced toward the producing side. This is a corporate-structure and legal question as much as it is an e-commerce question. The research named it as an option; it did not resolve it.

The longer route was the payment-rail policy change itself — the National Bank’s foreign-fintech registration requirements adapting to permit PayPal, Stripe, or equivalent rails to operate inside Kyrgyzstan without the full domestic-entity requirement. That is a policy timeline that the research did not control.

What the research could give the programme, and did give it, was the diagnostic: the products exist, the demand exists, the international marketplace is already selling Kyrgyz handicrafts at scale, and the gap between where the value is captured and where the value is created runs through a set of solvable — if not easily or quickly solvable — infrastructure and policy constraints. That is the starting point for the capacity work that follows.

— Aziz Soltobaev, KG Labs, October 2021.